At its meeting last week, FHLBank Topeka’s board of directors approved changes to its Member Products Policy. Details are available in the online Member Products and Services Guide and are effective April 1, 2025.

Lending Value Changes

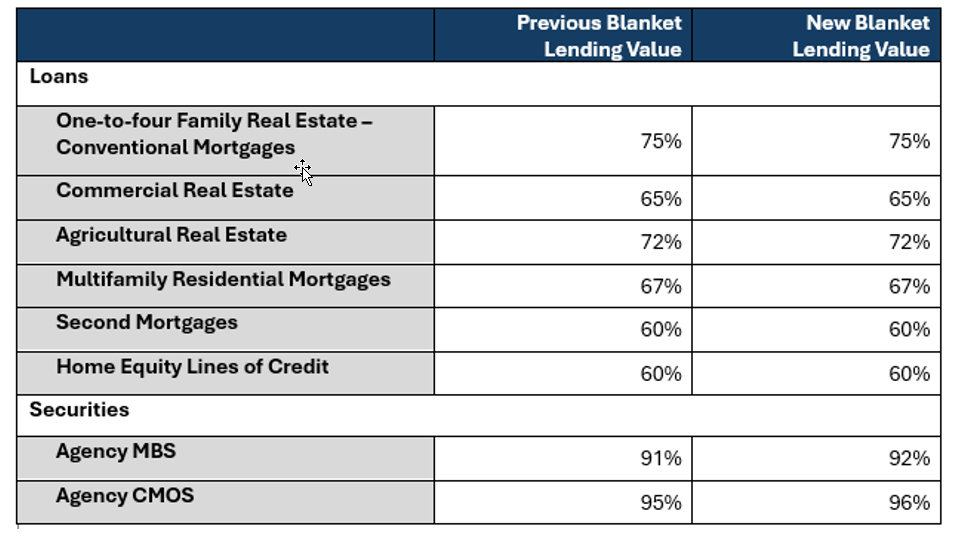

Lending values for a few mortgage loan categories and several securities categories are changing. As a reminder, the purpose of the assigned lending value is to ensure that if your cooperative must liquidate the collateral pledged (underlying securities or loans), sufficient remaining value from the sale of the loans or securities will cover a member’s outstanding obligations.

Lending values for most securities categories are slightly increasing due to a decline in market price volatility during 2024, while lending values for most mortgage loan categories are remaining stable. However, the lending value for multifamily real estate collateral pledged by specific pledge members is changing. In December 2024, FHLBank Topeka announced a reduction in the lending value from 74 to 67 percent for multifamily real estate collateral pledged by blanket pledge members.

A similar reduction in lending value for specific pledge members was approved by the board of directors during the March meeting resulting in reductions in the lending value for multifamily real estate collateral from 77 to 71 percent and 75 to 68 percent for Class A and Class B specific pledge members, respectively.

See the table below for a comparison of our most popular categories for the blanket (QCD) lending value. Visit our website for the full schedule of eligible collateral, including delivered (limited) and delivered (expanded) lending values.

Eligibility Change – Cure Period for One-to-Four Family Residential Real Estate Loans

For specific pledge members, the cure period (i.e., the period a loan must be current after being more than 60 days delinquent) for one-to-four family residential real estate loans has been changed from 12 months to three months. Please note, the cure period for multifamily residential mortgages and commercial real estate loans will remain at 12 months.

The purpose of this change is to delineate between the collateral categories in recognition that one-to-four family residential real estate loans cure differently than multifamily residential mortgages and commercial real estate loans. This change will not impact blanket pledge members as blanket pledge members have different delinquency eligibility requirements (i.e., loans cannot be more than 90 days delinquent).

Contact Us

If you have any questions, please contact Joshua Clark, chief credit officer, Tom Bliss, director of credit administration, or Dedra Duran-Gray, director of collateral and safekeeping operations, at 785.233.0507.